We Hit $150k in Debt on $13k a Month. Here's How.

At our peak, we owed almost $150,000, currently our household income is about $13,600 a month.

I know those two sentences don't seem like they belong together. How the hell did we get into this mess with a good income? While we've knocked it down to about $133,000 as of the end of March 2026, it doesn't feel like real progress... yet.

My name is Nora. I work a full-time W-2 job, two freelance contracts on the side, and I'm rebuilding a content business I let go dormant in early 2025. My husband works full-time as a tax accountant. He's a veteran with disability income. Between the two of us, we bring home more money than either of us ever expected to make.

And we are drowning in debt.

How we got here

My husband and I did Financial Peace University in 2015, before we got married. We followed the baby steps. We were debt-free except for a mortgage when we moved into our current house in 2023.

That house is my childhood home. I bought it from my parents. More on that in a future post, because that decision alone could fill a page.

After we moved in, things started stacking up. The house needed work. We had health issues that weren't cheap. I went part-time for a while, and our income dropped. And then there were spending decisions that just weren't smart. Not dramatic, not scandalous. Just slowly piling on the poor choices that added up fast.

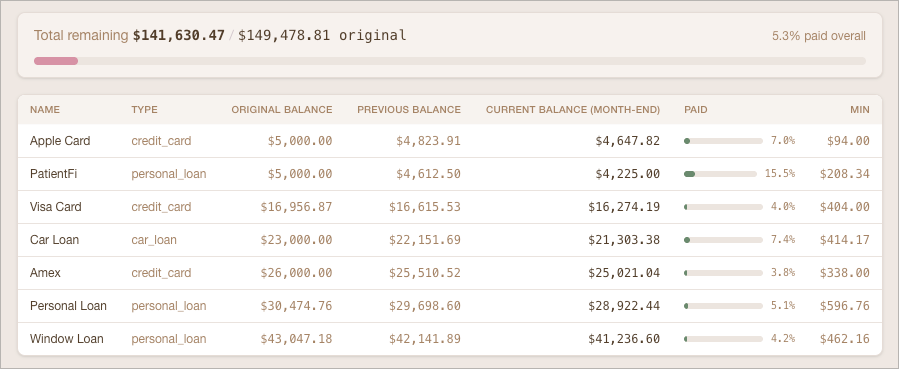

By the time I actually sat down and added everything up, we were at almost $150,000 in debt.

Every debt, line by line

I'm sharing the full breakdown because vague numbers don't help anyone. If I'm going to talk about paying this off, you should see what "this" actually looks like.

Here's the exact breakdown as of Jan 2026:

You might notice there are no student loans. We paid those off in 2022. That fact surprises people, because $150k without student loans means every dollar of this came from life decisions, not education costs. This would all be considered "bad debt," and it doesn't even include our $600k+ mortgage loan.

You might notice there are no student loans. We paid those off in 2022. That fact surprises people, because $150k without student loans means every dollar of this came from life decisions, not education costs. This would all be considered "bad debt," and it doesn't even include our $600k+ mortgage loan.

Good salary =/= Good finances

This is the thing I want to be really clear about, because it's the entire reason this blog exists.

Income is not the problem.

We've made $3,200 a month and felt broke. We now make $13,600 a month and still feel broke. The dollar amount on the paycheck changed. The feeling didn't. We let lifestyle creep ruin our finances. We should be in a really great financial position at this stage of our lives, given all the work we've done previously, but instead we've dug ourselves back into a hole.

When I tell people our income, I get one of two reactions. The first is "Well, you'll be fine then." The second is "how is that even possible?" Both of those reactions miss the point.

The problem was never the paycheck. The problem was the budget. Or, more accurately, the absence of one. The problem was looking at payments we could afford and not thinking about the stress that comes when we lose a job, have an emergency, or the interest starts piling up.

We stopped being intentional. We knew the money was there, so we assumed it would cover everything. It didn't. Money without a plan just disappears. It doesn't matter if it's $2,000 a month or $15,000.

I'm not writing this to get sympathy. I'm writing it because I spent years reading income reports from creators who made it sound like earning more was the answer. Earn more, pay off debt, build wealth, repeat. And for a while, I believed it. But we earned more, and the debt grew too.

What we're doing about it

We're going back to basics. Budgeting every single dollar. Track every expense. Attack the debt with a plan - and do all of this very publicly so that hopefully you can learn from my ups and downs, all while I have some serious accountability.

I'm going to document the whole thing here. Real numbers, real timelines, real setbacks. Not a highlight reel. Not a victory lap at the end. The actual messy middle, while we're still in it.

Every month I'll post what we paid off, what we spent, and what went wrong. Because something always goes wrong. That's not a failure. That's just life with kids, pets, a house that needs things, and two people who are still learning to manage money even though the world says we should know better by now.

If you want to follow along, sign up for the newsletter. I send updates there first, and I'm more detailed in my emails than anywhere else.

This isn't an advice blog. I'm not qualified to tell anyone what to do with their money. This is a documentation project. I'm going to show you exactly what happens when two people who make good money decide to actually deal with six-figures in debt, out loud, in public.

It might work. It might be embarrassing. Either way, you'll know.